Last 28 May 2026, Finance Minister Nicola Willis delivered the 2026 Budget. I won’t go into the details of the non-tax matters, as other commentators will cover this at length.

Tax barely featured in Minister Willis’ speech. In fact, tax was literally the last thing she covered before her closing remarks.

Minister Willis briefly mentioned the following tax matters:

- Changes to taxation of charities; and

- Simplifying FBT for motor vehicles; and

- Treating a loan left owing to a shareholder as taxable 6 months after the liquidation of a company; and

- A $200m levy on banks

The first three of these had been subject to consultation, although the final changes are not 100% in line with the consultation.

There were actually several other items that were not included in Minister Willis’ speech.

Here is a rundown of tax-related changes that will be introduced:

Charities/not for profits

The Government and IRD have been consulting for some time around potential changes to the taxation of charities and not-for-profits. The final changes seem to have addressed the concerns of overreach from some earlier proposals.

Key changes include:

- Increasing the amount of net income a not-for-profit organisation can earn without paying tax from $1,000 to $10,000. This threshold had not changed in almost 50 years.

- Ensuring the donation tax credit scheme remains financially sustainable by capping eligible donations at $100,000 per year. This will also limit tax planning risks that can arise when a donor makes a gift to a charity they control themselves.

- Allowing donors to receive their donation tax credit refunds throughout the year in certain circumstances, rather than waiting until the end of the tax year.

- Allowing donors to gift their donation tax credit to a charity.

- Ensuring that membership subscriptions and levies received by not-for-profits remain non-taxable. This overrides an unintended consequence of the adoption of a new Incorporated Societies Act.

- Charities and not-for-profit organisations with income of less than $10,000 will not have to file a tax return.

- Not-resident charities will no longer be able to be tax exempt in New Zealand.

Company loans to shareholders

Just before Christmas, the IRD released an extremely controversial paper on loans from companies to shareholders.

Thankfully, the Government has not adopted the full proposal and is instead only looking to tax the value of an outstanding loan left owing by a shareholder 6-months after the company is removed. This proposal is entirely sensible.

FIF rules changes

A surprise change, and one that was not mentioned in Minister Willis’ speech, is some changes to the Foreign Investment Fund or FIF rules. These are the rules that apply to New Zealand tax residents holding shares in widely-held foreign companies (other than the Australian ASX).

Upcoming changes to the FIF rules include:

- Increasing the de minimis for the application of the FIF rules for individuals from $50,000 to $100,000;

- Allowing anyone to use the recently introduced “revenue account method” or RAM method for unlisted shares. This was previously only available to new migrants.

Financial arrangement changes for new migrants

Another change that was not mentioned by Minister Willis is some measures to relieve the impact of foreign exchange gains and losses under the financial arrangement rules for new migrants. The financial arrangement rules create some unexpected outcomes for new migrants, as New Zealand is very unique in the way that we tax foreign exchange gains and losses.

These changes are a direct result of the consultation around the introduction of the FIF RAM method earlier this year.

The exact details of the changes were not published at the time of writing this article.

Non-resident contractors’ tax

Non-resident contractors’ tax or NRCT, is rather niche, overly complicated, and often overlooked. The Government has announced that the threshold for NRCT to apply increases from contracts earning $15,000 to contracts earning $75,000. This will reduce the scope of NRCT dramatically and better target it to where it should actually apply.

Research and development tax credits

The rules for research and development tax credits or RDTI, are being expanded/relaxed even more. New changes include in-year payments and relaxed deadlines.

On the other hand, the cap for internally generated software decreases dramatically from $25m to $3m.

Last but not least…FBT changes

A long-awaited overhaul of FBT has finally been announced (sort of). An overhaul of FBT was recommended in 2022, and consultation occurred last year. These changes were supposed to have been passed last year, but were delayed due to some unexpected pushback from the rural community.

The changes apply from 1 April 2027.

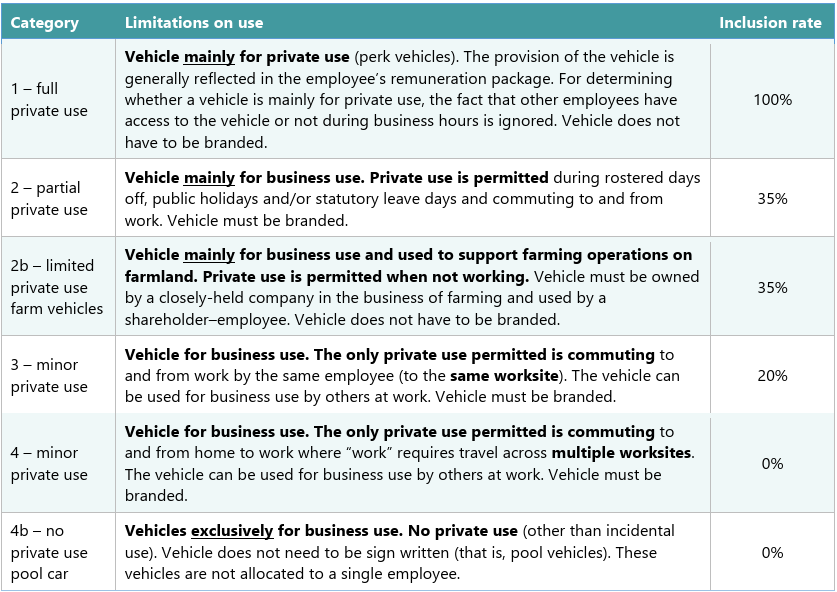

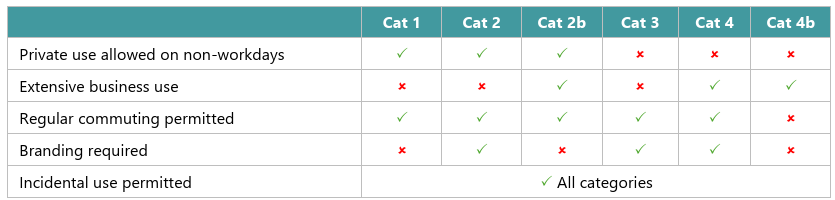

At the moment, the announced changes relate only to FBT on motor vehicles. The way FBT is calculated on vehicles is being simplified. The concepts of “available for private use” and “work-related vehicles” are gone, and instead the FBT will be determined by the way the vehicle is typically used. Vehicles available to employees will fit into one of the categories below:

The calculation of FBT will be far simpler now because there is no counting of days – the FBT is simply based on the category above.

Here is the IRD’s summary of what type of use is allowed for each category:

No announcement has been made on changes to the rest of the FBT rules. Exemptions had been expected for low-value fringe benefits.